Supply Chain Management and Logistics Blog. Posts are about end-to-end supply chain management and logistics in a time of challenging disruption.

Tom provides leading supply chain management and logistics consulting and advisory assistance based on real-world experience.

He brings authority and domain expertise to clients.

Email Tom at: tomc@ltdmgmt.com

Check Tom's profile at: https://www.linkedin.com/in/tomcraig1/

Do manufacturers struggle with e-commerce because they do not understand Supply Chain Management's strategic role? A change from what they are used to?

Beginning of dialog window. Escape will cancel and close the window.

0:150:15

The Key Takeaways From Nike's First-Quarter Earnings

The Key Takeaways From Nike's First-Quarter Earnings

x

Share

Embed

Permalink

The Key Takeaways From Nike's First-Quarter Earnings

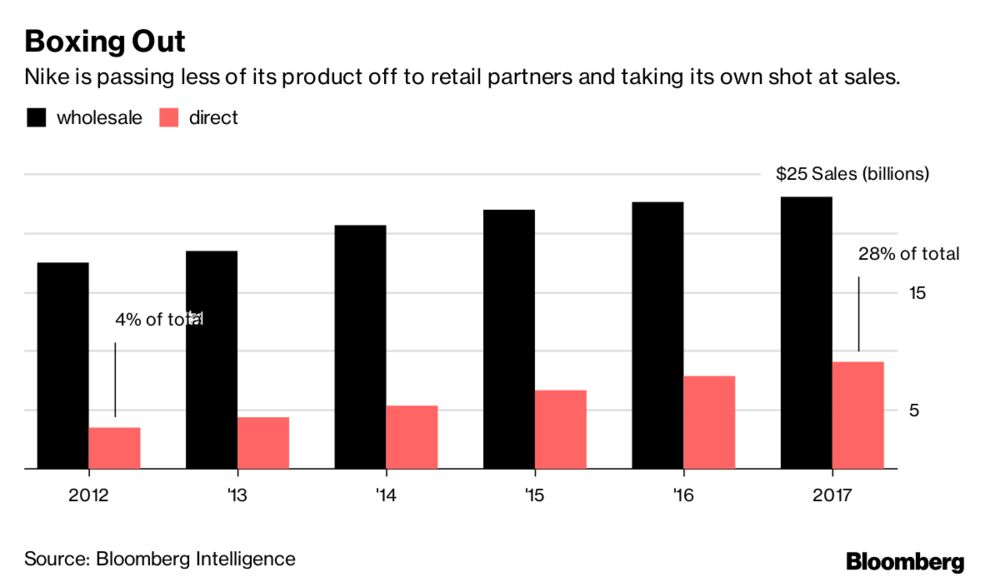

Nike started cleaning up its stats sheet Tuesday. For the first time, the sneaker empire declined to report “future orders,” a critical measure of wholesale demand from the galaxy of retailers who sell the famous kicks. The Swoosh says the metric doesn’t matter much anymore, because now it’s focused on doing business directly with consumers and cutting out the middleman.

While Nike reported its slowest quarterly sales growth since 2010, its performance as a retailer—rather than a wholesaler—was a relative highlight. Sales on Nike’s own web store were up 19 percent in the recent quarter, while its retail locations notched a 5 percent gain in same-store sales. Chief Executive Officer Mark Parker said the company is obsessed right now with making shopping more personal. “Retailers who don’t embrace distinction will be left behind,” he warned on a conference call Tuesday.

Still, that wasn’t enough to impress investors—at least, not yet.

The overlooked beauty of brick-and-mortar retail is how well retail chains lend themselves to what economists call price segmentation. Shoemakers such as Nike can easily target customers by sending the right shoes to the right kind of store (think: first-class vs. coach, iPhone X vs. iPhone 8, Banana Republic vs. Old Navy). In Nike’s case, it ships expensive, limited edition sneakers to high-end boutiques, routes its stock Jordans to chains like Foot Locker Retail Inc., and dumps its low-end product and off-key colorways in such places as DSW Inc.

If done correctly, all this socioeconomic slotting moves as much merchandise as possible with minimal fuss, while not tarnishing the larger brand. And make no mistake: Nike does it correctly. On its face, the Swoosh is a design shop supercharged by the kind of storytelling its TV commercials, billboards and magazine ads are famous for. But Nike’s real genius isn’t marketing, it’s merchandising: knowing exactly what to ship where. For every sneaker sketching savant in Beaverton, Oregon, there’s a mid-level manager with a giant spreadsheet, making sure “Momofuku” Dunks aren’t too easy to find, ordering up a special design for China, distributing its best-sellers to all the right Dick’s Sporting Goods Inc. outlets and dumping plenty of Chuck Taylors at outlet malls.

Mark Parker, Nike’s chief executive officer.

Photographer: Natalie Behring/Bloomberg

Nike is now upsetting its own well-oiled applecart. In giving traditional retail the stiff arm, which Nike made official in June, the Oregon empire is tearing up that playbook and trying to make an end run around the basic economics of price segmentation. The strategy—a bold move, given the historical manufacturer-to-retail model being discarded—requires no shortage of swagger. But Nike’s numbers show that the bet appears to be working, primarily because Nike has been sharpening its digital game.

Sought-after sneakers now ship out via Nike’s own ecosystem of apps, including SNKRS, which it launched early last year. The heart of its lineup, meanwhile, sells on Nike.com and in its own big box stores. As for the cheaper, less-popular kicks, they quietly trickle into the company’s “factory” stores (read: outlet) and onto Amazon.com. Nike even has a studio in New York that makes customized shoes on-site in about an hour.

In short, the company is deemphasizing its ready made network of retailers to create an even more precise targeting mechanism.

Yesterday, Parker said the end goal is to get ahead of the consumer and offer “the most personal, digitally connected experiences” in the industry. “While changing your approach is never easy, Nike has proven before that when we do, it’s always ignited the next phase of growth for our company,” he explained.

In theory, Nike can know any given customer better—and his or her willingness to pay—by using its own venues and platforms, particularly on its digital properties. The challenge will be building the mechanism to sort all the data, and in doing so, the customers. In the real world, they sort themselves: The high-end boutique isn’t right next to the cut-rate discount outlet. In the virtual world, it’s not so easy.

For the record, Under Armour Inc. is slightly ahead of Nike Inc., with 31 percent of its sales coming directly from consumers; Adidas AG is slightly behind, with 23 percent of revenue from retail. At its current pace, Nike will soon be collecting one in three of its sales dollars directly from consumers. Its challenge will be making that none of them get too good a deal.

Alibaba's 5 year logistics plan. Add Amazon & other e-tailers who are defining the future of retailing, logistics, and supply chains management. And the retailers who did not step up with supply chain management as strategic and invested in them...... Watching their futures in the rear view mirror?

"SupplyChain" is an oft-used and misused term by some tech firms and by logistics providers. What they call supply chain management is really logistics.

E-commerce fulfillment risk for laggard retailers, manufacturers, 3PLs. Risk of Amazon Effect and being Amazoned. The competitive point is moving continuously. Delay increases the distance behind.

When will 3PLs and providers wake up? Or will it be too late when they begin to try? And outsourcing risk?

MORGAN STANLEY: Here are the 4 industries Wall Street thinks Amazon will destroy the fastest (AMZN)

Seth Archer

Sep. 22, 2017, 11:12 AM

You've probably heard the term "Amazoned" recently. It refers to Amazon's power to erase billions of dollars of competitor market cap by simply announcing that it's entering a new sector.

It's an effect most clearly demonstrated by Amazon's recent acquisition of Whole Foods, which has sent shockwaves across competing grocery stores, brick-and-mortar retailers, and even pharmacies.

To see how far this Amazon effect will go, analysts at Morgan Stanley surveyed their peers to see which sectors will be the most impacted by Amazon in the near- and long-term.

Most analysts surveyed, more than 40 in total, said that food retail would be the sector hit the hardest. Amazon entering the food retail space through its Whole Foods purchase has already erased billions from grocer's market caps.

In second place were department stores, with 49% of analysts saying that's the sector Amazon would disrupt the most in the next 12 months. This makes sense as consumer habits have been shifting towards ecommerce amid the retail apocalypse.

In the non-consumer space, Wall Street sees logistics and transportation as the most vulnerable to Amazon, with 43% of analysts voting for this option. Retail real estate investment trusts came in second, with 36% of the vote. Amazon owns significantly less warehouse space than people think, with Walmart way out in front by that measure. The Whole Foods purchase adds about 1 million square feet of space to Amazon's warehouse holdings, but the company is looking to expand, which analysts think could upset the retail real estate industry.

Morgan Stanley's survey also asked analysts about which industries were mostly safe from Amazon's reach. They replied saying dollar stores would take the longest for Amazon to disrupt in the consumer space, while healthcare and commercial REITs would be the safest in the non-consumer space.

As for the sector that has been the most unfairly impacted by Amazon? Well, that would be auto parts retailers, according to those surveyed.

Shares of Amazon are up 27.55% this year.

Issue with integrated global trade, logistics, technology, supply chain, finance platform is decentralized/transaction client vs centralized/performance.

In May 2015, I argued that it was hard to find cracks in the way CH Robinson was run, observing that the US-headquartered 3PL had historically demonstrated sound financial discipline – but, “nonetheless”, I also noted, “delving into its financials and its stock performance, it appears to have arrived at a crossroads”.

At the time, its stock traded in the mid-$60s, much the same as its level on 20 July this year, when it hit a 52-week low of $63.4 in the wake of its interim results. Two months later some of its financial hurdles have become hard to overlook, at least judging by its performance in the six months ended 30 June, and given underlying trends for asset-light businesses so far in the third quarter.

CHRW Net revenue and earnings (source CHRW)

Turning point

In the past eight weeks, its shares have looked for direction, rallying well above $70 – where they currently trade – on two occasions. However, when they surge above that key level, they become more unpredictable and volatile.

CHRW Share price (source Yahoo Finance)

Of course, in today’s world of advanced, cloud-based IT solutions, the very role of 3PLs and 4PLs is more openly questioned than in the past, which might have something to with its stock price volatility. However, in CH Robinson’s particular case, the chief culprit appears to be investors becoming increasingly wary of declining profitability and, more broadly, significantly less profitable volumes.

CH Robinson, of course, has a pedigree of experience that few can match, but “Silicon Valley will continue to drive prices down and as you know, forwarders and employee-heavy businesses such as CHRW need rising rates and oil prices to boost margins”, freight forwarding veteran Steve Walker, owner of SWGlobal, told me last week.

Moreover, he insisted that “current changes are beyond what the management systems of 3PLs can handle”.

While there are certainly indications that how IT affairs are managed is changing in the industry, that fact is that the threat of substitutes and the risk posed by potential entrants (see Porter’s Five Forces) comes at a time when financial risk is also alive and well, as proven by the latest results of CH Robinson and those of several of its global peers.

Additionally, stock prices trends need to be taken into account. Bellwether

Technical analysts would likely argue that a much lower valuation, in the low $60s, is another key support level.

Charts are often reliable only in hindsight, but $61-63 is a trading range worth watching carefully because if CH Robinson’s stock drops 15% or so from its current level, it is key indication of deep structural problems, not only with a bellwether company in the North American logistics industry, but also with other transport intermediaries in Europe and Asia, where many players are coping with very unfavourable pricing/volume dynamics inherited from their shippers. Sugar high

While it is true that, in February, CHRW reached a record high of about $80, the observation that the company appeared on a more solid footing ignored one basic element: share prices are seldom rational.

In fact, its shares – as with many other stocks in logistics – were boosted by the Trump effect for about six months, how weird that might seem, but it allowed CHRW investors to ignore the first symptoms of deteriorating fundamentals. And in the meantime, these have been offset by an attractive yield from dividends, although benchmark yields (US Treasury and others) continued to rise.

I labelled CH Robinson as a safe haven in February 2016, when its stock traded a tad below $70, but I am not so sure anymore, particularly because dividends could rise at lower clip over the medium term than in recent quarters.

CHRW dividends history and growth (source CHRW)

I am also less optimistic than I was in July 2016, when again it traded around $69, with the first signs of stress becoming increasingly evident in the first quarter this year, although in my latest coverage, in March 2017, I acknowledged the company was changing. Trends

In short, dividend growth could be a stumbling block.

While the projected payout ratio is safe, it will likely rise closer to 60% this year from 48% in 2016, based on consensus estimates from Thomson Reuters. It was well below 50% between 2014 and 2016.

One problem with CH Robinson is common to many other 3PLs: variable and fixed costs are rising at a faster pace than in the recent past as gauged against net revenue growth, inevitably biting into their bottom lines. Which, in turn, impacts cash flows, rendering dividend payments heavier.

Under these circumstances, companies need other sources of funding to support certain cash outlays such dividends and buybacks.

And here is how things look at CH Robinson: operating cash flow in the first half of 2017 fell a whopping 40% to $150m from $247m one year earlier.

CHRW operating cash flow 1H (source CHRW)

By comparison, its annualised figures between 2014 and 2016 are shown in the table below.

CHRW operating cash flow 2014-2016 (source CHRW)

Needless to say, perhaps, second-half results will have to be stellar to provide some relief, or even just to maintain the payout in the safe zone. Funding mix on the radar

Unsurprisingly, CH Robinson decided to stick to a conservative approach to heavy investment (capex) in the first half, but given lowly capex requirements as a percentage of revenues and against core cash flows, even significantly higher cash outlays from investment would have been just a nuisance.

Notably, though, borrowing was a precious source of funding, shoring up its rising cash position at the end of the first half. However, without external debt, maintaining a rich dividends and buybacks policy would have been impossible, my calculations suggest.

Borrowings, buybacks, dividends (source CHRW)

A little detail – there is a $250m of cash inflow from a receivable securitisation facility, its cash flow from financing showed at the end of June. Clearly, such borrowings are just part of normal cash flow management activities, given a lowly net leverage of about 1x, but it is also legitimate to question whether we should expect more to see debt sitting on its books, say, in a year’s time.

For the time being, at least, I wouldn’t feel uncomfortable if my name was on the shareholder register, but new debt is one variable to watch – given steady outlays from cash from financing, either cash flows surge or the dividends and buybacks will have to fall. It could be better – or worse…

Not only are costs rising…

P&L: gross revenues vs COGS (source CHRW)

…but the headcount is up…

Headcount (source CHRW)

…which brings higher operating costs and SG&A expenses.

Operating costs growth (source CHRW)

Inevitably, too, its underlying projected profitability is expected to hover below trend in the near future.

Income statement evolution (source 4-traders.com)

Tech component

The company recently acquired a tiny forwarder in Canada, which doesn’t move the needle in terms of earnings accretion, as CH Robinson accepted.

Meanwhile, if you are familiar with its corporate affairs, you’ll probably know that transformational deals are off the radar.

Quite frankly, I do not know what the solution for this is, and for other asset-light freight forwarders and truck brokers, but the tech component of its offering to shippers will surely be key value-driver.

Mr Walker pointed out that CH Robinson was no different from all other leading players in the field which offer services that are essential for supply chain management activities, but increasingly it appears that these can be easily replaced – over time – by cheaper, automated alternatives.

“It is all about business intelligence. If you asked 3PL executives what keeps them awake at night, the common thread would be IT solutions (…) in a marketplace where the freight forwarders, in particular, need to cut costs. Yes, to cut the headcount further, but not many can do that”, given the typical correlation between growth and staff investment in the industry.

Essentially it is about doing more with less, as well as paying more attention to internal processes and “compliance – and many players realise they have little control over it”.

“Their customers want more, so the middle man needs to change its model. It is no longer logistics, in a way, it’s about independent 4PL reporting, and feeds.”

Mr Walker kindly flagged me the latest product release of CH Robinson: last week it launched Navisphere® Vision, “a supply chain technology that provides real-time global visibility across all modes and regions in one platform”.

Navisphere® Vision

It is certainly encouraging, but there is also no hard evidence that its latest cash flows will buck the trend thanks to its contribution, making me wonder whether the possible reward is really worth the risk for shareholders at these levels.

Is finance one of the reasons that retailers and manufacturers have not transformed their supply chains to deliver the e-commerce customer expectation?

The behaviour of the Hapag-Lloyd share price since late 2016 proves the bulls in container shipping circles may be right in largely ignoring the risks surrounding the sector’s leading players, which continue to show optimism after a solid start to the year.

Hapag share price (source Yahoo Finance)

The fundamentals of the German carrier, however, suggest that if a best-case scenario doesn’t play out, and rate levels become more difficult to maintain, the recently drafted optimistic scenarios could become a nightmare as soon as 2019 for its worldwide network, making it one of the most obvious takeover targets in the industry.

Hapag network (source Hapag)

Down, up, and down

At the end of June 2016, when its shares still traded below the IPO price of €20, the German carrier announced its merger agreement with United Arab Shipping Company and took the lead in a consolidation game that has since seen a slew of M&A deals concluding with Cosco striking the most expensive acquisition in liner history via its OOCL acquisition.

Before tie-up rumours emerged in April 2016, the stock of Hapag traded around €16. It now changes hands at €37, mainly thanks to that deal.

The demise of Hanjin and tighter capacity came to the rescue on the back of a fast-consolidating market, transforming what was a dreadful investment for over a year – as I expected when Hapag was about to price its IPO in late 2015 – into a spectacularly high-yielding investment since the turn of 2016.

With hindsight, Hapag management embraced the only strategy it could entertain at the time, doing all they could to prevent a painfully slow death. Thanks should also go to its bankers, who have little choice but to help the company stay afloat, given the billions they are owed. But where does all this leave Hapag now? And who will end up being the ultimate winner?

Hapag itself could well be answer, I reckon. Outlook

Freight rates per trade arguably played in favour of the Hapag/UASC tie-up in the first half, as the chart below shows.

Freight rates per trade (source Hapag)

The same applies to the development of global container fleet capacity…

Global container fleet capacity (source Hapag)

…as well as volume trends, which boosted Hapag’s top-line even before the consolidation of UASC was taken into account.

Transport volume per trade (source Hapag)

Revenue per trade (source Hapag)

Based on all these elements, it is unsurprising that its shares trade at record levels of €38, which suggests financial investors continue to be happy to buy into a positive outlook for shipping lines – a view that is also shared by several sources in the liner industry I talked to recently.

Meanwhile, new orders for ultra-large container vessels are also encouraging, right?

Hapag has emerged in a more dominant position thanks to rising freight rates and a lack of alternatives on the routes it serves – however, their contribution to its interim P&L figures was more of a marginal embellishment than substantial gain.

And the balance asset, where assets and liabilities are booked, doesn’t look great either, although analysts at Moody’s and sell-side brokers think otherwise, given their projections. Growth

While Hapag management talks of “qualitatively enhanced growth”, its earnings quality has deteriorated, in my view; and surely how that growth is financed is equally important.

Sustainable growth (Source: Hapag)

Of course, Hapag minimises certain risks, saying that global GDP growth will accelerate above trends in the next 15 months or so, with volumes comfortably outpacing global economic growth…

Economic outlook (Source: Hapag)

The message here is clear: the economy will be the silver bullet the container shipping industry needs at a time when the main players consolidate at the fastest pace in history, determining different pricing dynamics along the value chain that, ultimately, will favour the top five carriers.

Currently, Hapag remains the smallest, and the most vulnerable, based on its current financial situation.

Top five market share (Source: Alphaliner)

(A quick digression on the economy: you may not have noticed, but earlier this month the 10-year US Treasury yield hit its lowest level of 2.05% for 2017, down almost 60 basis points from its highest point – induced by the Trump rally – which says a lot about subdued growth prospects for the world’s largest economy, and hence for the rest of the world. Additionally, it is convenient to ignore that the bull market is almost nine years old, while benchmark indices continue to record new highs on a daily basis – however, as latent recessionary forces persist globally, a double-dip in the container shipping industry cannot be ruled out given that the worst year on record for the ocean carriers was little more than nine months ago.) Debt

I have recently warned you that debt trends were not good, either for Hapag nor the broader industry.

The fact that credit rating agency Moody’s recently placed the rating of Maersk under scrutiny is only a minor event, though – the market leader, even following a possible downgrade, will remain in investment grade territory. Based on its current credit rating, it currently ranks two notches above junk.

Hapag credit rating chart (source: Hapag)

The stock of the Danish behemoth shrugged off the news, but Hapag is an entirely different story, because its balance sheet is significantly more stretched and its credit rating deep in junk territory.

Credit rating grid (source: Moneyland.ch)

It is possible that Moody’s is right and, if so, in less than two years the German carrier will have materially improved its financial status.

Moody’s forward view for Hapag/UASC (source Moody’s)

After all, its free cash flow profile received a fillip at the end of the first half…

Hapag free cash flow (source Hapag)

… and capex requirements will inevitably fall based on historic standards following the UASC integration (although, inevitably, its vessels will be older than rivals reportedly looking to place new orders).

Furthermore, some key returns figures were better than previously, as the chart below shows.

Snapshot financials (source Hapag)

But the same table above also includes its total financial indebtedness – and that should raise eyebrows, having risen 78% to €7.3bn following the consolidation of UASC, while borrowed capital, which includes other liabilities, is even higher.

Hapag also consolidated additional cash and earnings of UASC when it acquired it – but it’s too early to know whether the deal was actually worth it. Little improvement in first-half ROIC (return on invested capital) metrics – which gauge how efficiently capital is deployed and is a key yardstick for Maersk’s management – prove my point.

Hapag return on invested capital (source : Hapag)

Meanwhile, a tiny free float makes it all riskier for shareholders who are invested, one could argue. Although if a bear-case scenario plays out and the bulls are wrong, that might only be a minor concern.

Hapag shareholder structure, including free float (source: Hapag)

Because then, Hapag – which for so many years was tipped to merge with Hamburg Süd before Maersk swooped – could easily become a target for Maersk once that line’s restructuring is complete, say, in 2019. It wouldn’t come cheap, and could well spark a bidding war.

When asked about the likelihood of Hapag being acquired by Maersk eventually, several executives, who I am grateful to for sharing their views on shipping market trends in recent weeks, agreed: “Such a combination would make a lot sense.”

Markets Insider

Markets Insider