Analysis: Expeditors the next takeover target for DP-DHL?

Market conditions

Oh yes, I am looking forward to sifting through the full financial results of the German behemoth next week. But briefly, it is important to flag certain warning signs in its trading update, dated 8 March, which shows a falling top line for DHL Global Forwarding (DGF) – down €1.15bn to €13bn, or 8.2% year-on-year – by far the largest fall since the €3bn top-line drop DGF experienced in the aftermath of the credit crunch, in 2009.

Management in Bonn is bullish, as DGF’s annual operating income rose swiftly, hitting €287m (compared with 2015’s €181m loss), but the impressive yearly surge was only due to heavy one-off charges (basically, the now-infamous bill for the New Forwarding Environment IT disaster) that pushed the unit into the red in 2015. In fact, DGF’s Ebit still remains shockingly below previous years’ levels (2014: €293m; 2013: €478m; 2012: €514m; 2011: €440m).

Bad mix

Undoubtedly, these are difficult times for most players. Currency headwinds are combining with a deflationary, more competitive environment, which is also characterised by lower oil prices – “Oil breaks below $50 a barrel for first time in 2017” was a recent headline in MarketWatch.

This does not help global logistics operators, so it is almost inevitable to speculate that cash-rich forwarders could attract interest from third parties, particularly rivals that are bigger and more diversified.

Expeditors International of Washington, one of the healthiest and most profitable companies in the field, has been high on my radar since it reported annual results at the end of last month. I am now publicly speculating: could it actually be a target for DGF?

A deal would cost $15bn for its equity, I reckon, implying a 50% premium to its current market cap – it is certainly do-able, but what are the odds?

Crown jewel

Expeditors is a crown jewel in the freight forwarding universe, but I gather certain figures sent shivers down the spine of some value investors and its stock has essentially been flat since it disclosed its financial performance on 21 February.

(To learn more, about the company’s business lines and prospects, please read this comprehensive article here.)

After a solid 2016, which came in the wake of another record year in terms of financial performance, Expeditors has some serious decisions to make. It trails the market leaders by some distance, both in air and sea freight, and the odds have to be long that the gap will narrow significantly anytime soon.

Organic growth is hard to come by, while it is also debatable whether the recent appointment of Philip Coughlin to the newly created post of chief strategy officer could end up being a defining moment. A company veteran with 31 years’ experience, Mr Coughlin fits with the track record of Expeditors, which leaves me – and you are entitled to feel the same – underwhelmed when it comes to creative capital deployment strategies.

Source: Expeditors

Traditionally shy in deal-making, the US forwarder has a tendency to avoid the M&A spotlight. However, a soaring gross cash pile, a conservative payout ratio and an under-levered balance sheet could prove to be more of a headache more than balm if it is serious about delivering incremental returns to shareholders this year and next.

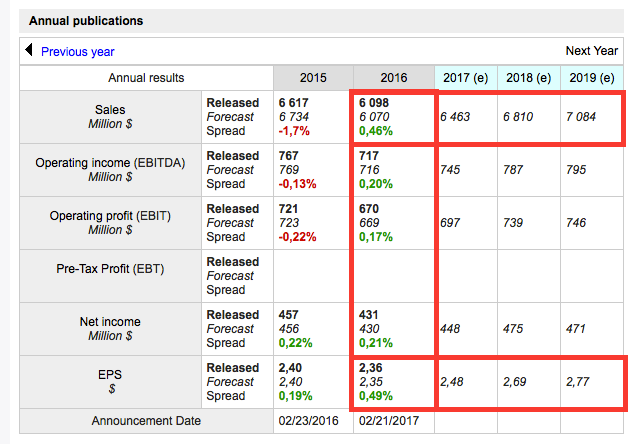

On the one hand, a timid stance on corporate strategy is understandable, given the sluggish business cycle and a lowly forward dividend yield in the 1.4%-1.5% area, which ought to be preserved, if not raised; but there remains downside risk to bullish projections for earnings per share and revenues, as the table below suggests.

Source: 4-traders.com

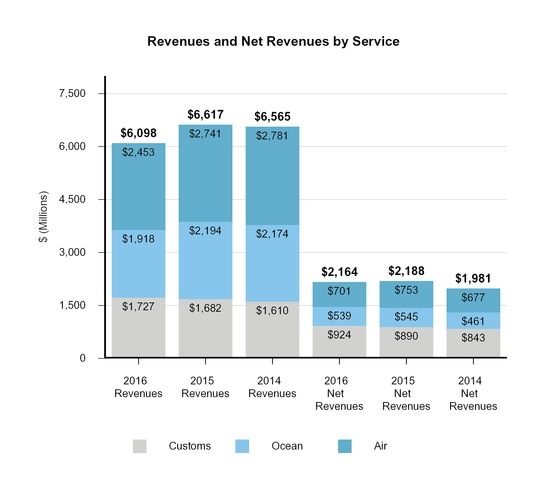

On an aggregate, gross and reported basis, the top line fell 7.8% year-on-year to $6bn, broadly in line with consensus estimates, while net revenue, a non-GAAP measure of performance, declined 1% to $2.16bn – which is the first time non-GAAP sales have dropped since 2012, when the fall to $1.83bn was more pronounced, admittedly.

Source: Expeditors’ 10k form

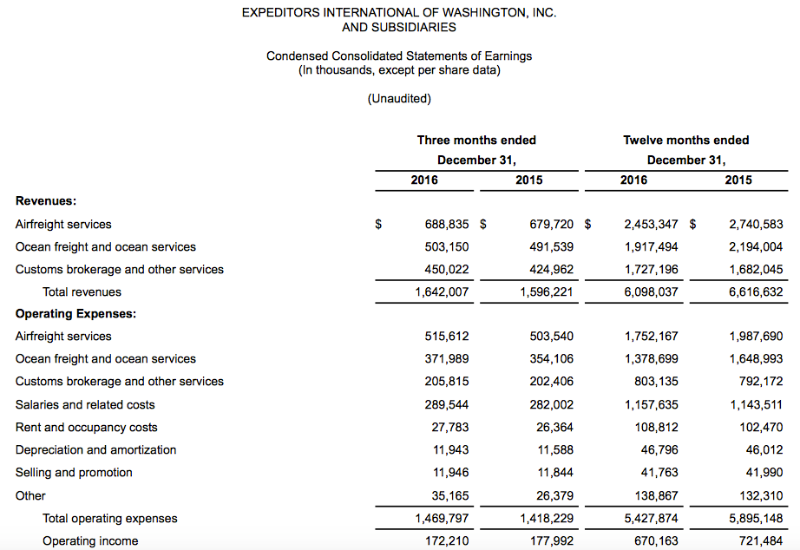

Expeditors stands out in the industry when it comes to costs management – direct and indirect expenses that are essential for its daily activities fell 7.9%, slightly outpacing the drop in gross revenues. Its largest cost, associated with ocean freight and ocean services, plunged 16.3% to $1.75bn, followed by an 11.8% decline to $1.37bn in air freight expenses.

Essentially, it is doing what sea freight leader Kuehne + Nagel does best: shoring up gross profit, while other operating costs are on the rise.

Source: Expeditors’ 10k form

On the fence

At operating level, its income was only $51m lower year-on-year, and although that fall represents 35% of annual dividends, and 15% of the cash spent on buybacks, it wasn’t material as Expeditors continues to manage working capital carefully.

A significant drop in cash inflows from receivables was fully offset by a drop in payables, and the amount of cash flow it churned out from operations was only $35m lower on a comparable basis – which again indicates near-flawless execution and financial ability.

Why on earth, then, would it need a partner or a takeover?

One for UPS

Shareholders enjoyed 16.6% pre-tax returns excluding dividends, but crucially, its five-year performance on a relative basis is less enticing.

Source: Expeditors’ 10k form

Source: Expeditors’ 10k form

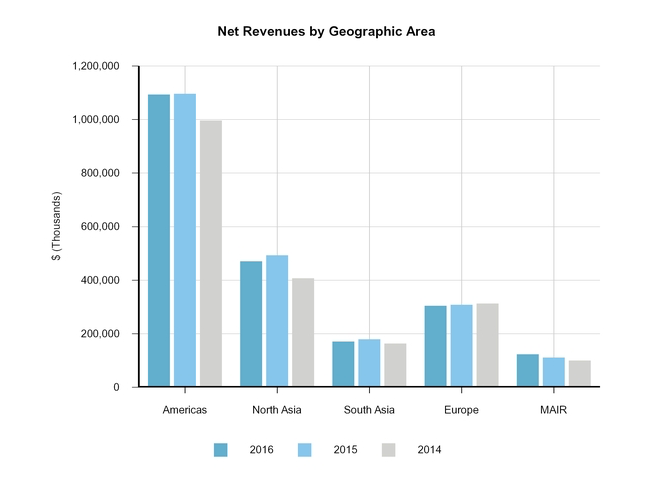

More broadly, the recent EU ruling concerning the aborted UPS/TNT merger deal of 2013 reinforces the view of some observers that Europe, where Expeditors also generates meaningful revenue, might again be a place to consider – although admittedly seeking strategic partnerships or deeper ties there does not seem a very smart idea, especially given latest remarks from the European Central Bank‘s chief, and in any case, only circumstantial evidence indicates that DGF would be attracted to Expeditors.

But it would make a lot of sense, in my view, to combine its sea freight activities, and perhaps even its air freight business, with closer rivals, such as DSV, Panalpina, Bolloré or Nippon Express, although the big issue here is that Expeditors would likely be the diner rather than the dinner, given its size.

Finally, to paraphrase the words of a London-based deal-maker, as protectionism prevails and the world becomes a smaller place, a blown-out offer – if one emerges – would have to be crafted by one of the major logistics companies in North America. In that respect, UPS, which has its own problems, could be the ideal acquirer – it ticks all the boxes financially and while its market share in sea freight is almost negligible worldwide, it ranks just outside the top 10 in global air freight.

No comments:

Post a Comment